Welcome to The Interchange! in case you acquired this in your inbox, thanks for signing up and your vote of confidence. in case you’re studying this as a submit on our website, be a part of right here so that you’d possibly receive it instantly finally. every week, I’ll try the most effectively appreciated fintech information of the earlier week. this will embody every thing from funding rounds to traits to an evaluation of a chosen space to scorching takes on a chosen agency or phenomenon. There’s pretty a little bit of fintech information on the market and it’s my job to protect on extreme of it — and make sense of it — so that you’d possibly preserve inside the know. — Mary Ann

Helloooo and glad New yr! Feels want it’s been a whereas since I sat proper down to jot down this textual content material. I’ve missed it!

earlier than I dive into the information, I needed to say that I hope you all had a restful and pleasing journey. Ours was great low-key however that’s not a foul factor. nonetheless, i will admit it has taken a bit for my mind to fluctuate again to work mode this week…so bear with me.

On Friday, I printed an article on Doorstead’s $21.5 million collection B enhance. The story was amongst the numerous most be taught on the positioning that day, extra proof that individuals are actually interested in expertise that pertains to the property rental market, particularly with reference to investing. For its half, Doorstead says it’s larger than a full-service property administration agency, in that it ensures the householders it actually works with a minimal quantity in lease. If it might’t get the quantity that it ensures, it can cough up the distinction. If it will get extra, effectively, the proprietor will get the extra — not the agency. Doorstead says it deliberately opted to solely earn money by charging an eight% administration payment so as that its incentives are aligned with that of the householders it actually works with. By being eager to pay the distinction, the agency says that it’s ready to scale again the interval of time rental properties sit vacant. So, householders will not be solely getting a assured rental income, however they’re additionally having their properties rented out faster and making extra money that method, the agency’s founders, Ryan Waliany and Jennifer Bronzo, say. Notably, Doorstead additionally introduced that it picked up the Boston property of one other enterprise-backed proptech, Knox monetary, whose enhance I had coated in 2021. I don’t have particulars as to what led to the latter agency winding down its operations, however i suppose we’ll be seeing extra of this sort of factor in 2023. And by “sort of factor” I imply startups buying property from completely different startups. to hearken to the equity Podcast crew’s ideas on Doorstead’s mannequin, head right here.

Over the break, we printed an interview that I had performed with GGV Capital’s Hans Tung and Robin Li by means of the fourth quarter. For the unacquainted, GGV is a enterprise agency with $9.2 billion in property underneath administration that invests in startups from seed to progress levels throughout a quantity of sectors, collectively with shopper, internet, enterprise/cloud and fintech. Some highlights of the interview embody Tung’s views on down rounds not being the extreme of the world. He informed me that he’d barely see a startup enhance a down spherical than shut down, and that what issues finally is the outcome. Refreshing! He additionally shared a quantity of the advice he’s giving to his personal portfolio firms, amongst completely different issues. in the meantime, Li provided her ideas on why embedded fintech will stay scorching.

whereas I’m constructive there have been already many down rounds in 2022, Tung expects we’ll see method extra in 2023 as startups that had raised in 2021 started to get low on money. I agree collectively with his view that there’s no disgrace in elevating a down spherical. Valuations had been overinflated and any down rounds which might even be introduced this yr are most usually reflecting valuations which might even be extra sensible and simpler to defend.

Doorstead co-founders Ryan Waliany (CEO) and Jennifer Bronzo (COO) picture credit: Doorstead

Weekly information

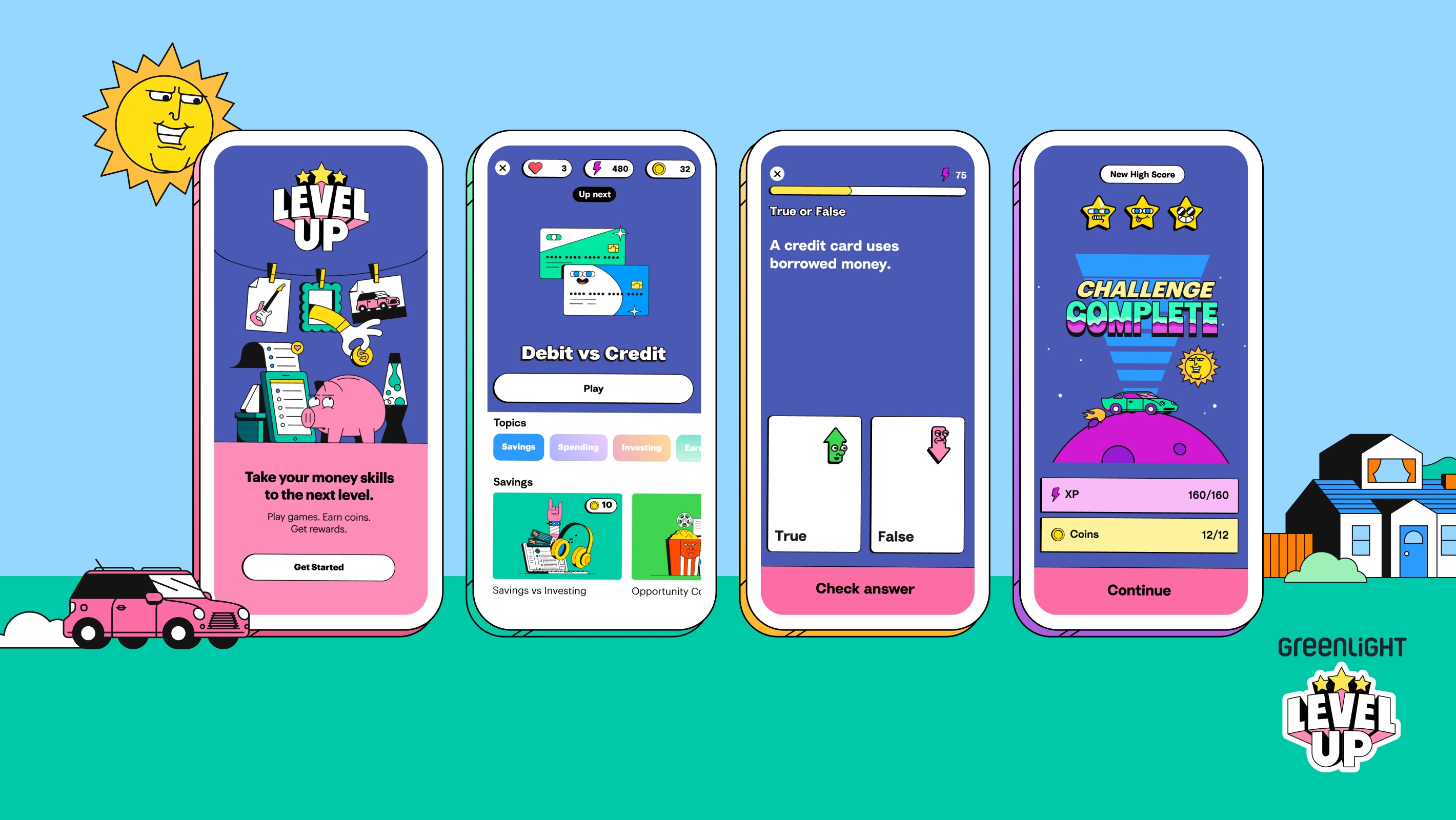

On January 6, self-described household fintech Greenlight launched Greenlight stage Up, an interactive, curriculum-based mostly monetary literacy recreation. Clearly the agency is attempting to enchantment to the youthful expertise’s love of taking half in video games digitally, although one has to marvel what took it so prolonged to incorporate a recreation in its offering. through e mail a spokesperson informed me: “kids can earn digital cash, expertise factors, and have interplay with exact-life money classes by means of dynamic graphics, story-pushed gameplay, and animations on their cell telephones or tablets — taking the ideas of gamification and making use of them to actually one of many important abilities they’ll want for his or her complete lives.” in fact, the gamification of funds isn’t a mannequin new idea. final yr, I wrote about Truist, actually one of many nation’s largest monetary institutions, buying fintech startup prolonged recreation in its efforts to enchantment to a youthful clientele.

BaaS startup Synctera mentioned it is teaming up with Wahed (that means “One” in Arabic), a digital Islamic funding platform that describes itself as a outcome of the world’s first halal funding app. Synctera says it is offering the infrastructure for Wahed to make its providers obtainable to the three.5 million residents of Muslim religion inside the U.S. Presently, Wahed has larger than 200,000 consumers inside the U.okay. and Malaysia and is using Synctera’s offering to assemble checking account merchandise and roll out a debit card program linked to its app for Muslim individuals. particularly, a Synctera spokesperson informed TechCrunch that “Wahed at present provides halal investments, structured in accordance with established Islamic ideas and requirements, to US prospects. With Synctera, Wahed might be ready to current their prospects with financial institution accounts (making funds swap simpler and smoother) and debit playing cards (for useful entry to funds).” Synctera CEO/founder Peter Hazlehurst wrote through e mail: “We’re actually excited to assist Wahed launch banking merchandise for his or her U.S. prospects….We count on to see a wave of mission-pushed firms like Wahed embrace embedded banking to assist people brighten their monetary futures.” in current occasions, we’ve seen more and more fintechs shaping their choices to cater to very particular demographics corresponding to Hispanics, Blacks, Asian individuals and immigrants usually. solely time will inform if that sort of area of curiosity focus will repay.

In that vein, Boston-based mostly Mendoza Ventures — which describes itself as “a feminine and Latinx-based fintech, AI, and cybersecurity enterprise capital agency” — introduced that it has achieved a principal shut on its $one hundred million fund — its third. sadly, the agency wouldn’t share how a lot it has raised to this point however did say in a press launch that the fund “will prioritize investing in early progress stage startups with a give consideration to various founding teams.” Hey, we’re always right here for any initiatives geared in the direction of elevating various founding teams. Notably, financial institution of America led the preliminary shut, which included participation from Grasshopper financial institution and completely different undisclosed buyers.

To kick off the yr, Felicis Ventures‘ managing director Victoria Treyger penned a visitor submit for TechCrunch, offering up her predictions and the place she sees alternatives inside the fintech space. in the meantime, Bessemer enterprise companions Charles Birnbaum informed us through e mail that he believes that “With FedNow lastly slated to launch extra broadly in mid-2023, all eyes might be on alternatives round faster funds. whereas adoption of the Clearing dwelling’s RTP scheme has been reasonable to this point, we count on FedNow’s use of the prevailing FedLine community to velocity up faster cost adoption starting in 2023. There might be pretty a little bit of alternative to assemble the enabling modern infrastructure to be used-cases like payroll, insurance coverage disbursements, supplier funds and extra and on the equipment layer for extra seamless b2b and shopper funds experiences.” He’s additionally nonetheless bullish on the continued institutional adoption of blockchain expertise in some large areas of monetary providers. for event, he predicts that SWIFT “will proceed to experiment with central financial institution digital currencies (CBDCs) whereas extra banks will be a part of the USDF Consortium to facilitate compliant swap of worth over blockchains through financial institution-minted tokenized deposit stablecoins.”

talking of blockchain, Mercuryo, a crypto-focused startup that has constructed a cross-border funds community, has now launched a BaaS reply, which it claims “unlocks a singular function — the vitality to handle banking and crypto accounts inside a single platform.” A spokesperson for the agency informed me through e mail the aim is to make it simpler for conventional banks to open crypto accounts for his or her prospects and to current crypto platforms an reply to open financial institution accounts which might permit their consumers to retailer, swap and pay in fiat/crypto. I coated the agency’s enhance in June of 2021.

It was cool to see a startup whose enhance I coated final yr be named a Time most interesting Invention of 2022. Altro raised $18 million final might to develop its offering, which goals to assist people construct credit rating by means of recurring cost kinds corresponding to digital subscriptions to Netflix, Spotify and Hulu. Personally, i am a fan of the startup’s inclusive credit rating-constructing efforts, which problem the antiquated credit rating rating mannequin right here inside the U.S.

final week, Darrell Etherington and Becca Szkutak had been joined by Brex co-founder and co-CEO Henrique Dubugras to chat about what made him and his co-founder, Pedro Franceschi, decide to launch the agency card agency and why the buddies, who met on-line as youngsters, decided to be co-CEOs, amongst completely different issues.

in conserving with pay transparency tracker full.io, Stripe isn’t precisely so clear about its pay. The fintech large does not embody wage ranges in its CA or NYC job posts. The tracker additionally found that a strategic account authorities at fintech startup Bolt could make — you ready for this? — $374,000 to $462,000 OTE/yr. (in case you’d see me, I’m making the Kevin in “dwelling Alone” shocked face proper now).

As reported by Manish Singh: “Suhail Sameer, the chief authorities of BharatPe, will go away the most interesting position later this week as a outcome of the Indian fintech startup scrambles to steer the ship after kicking out its founder final yr for allegedly misusing agency funds.” extra right here.

picture credit: Greenlight

Fundings and M&A

whereas we’re not seeing many megarounds inside the fintech space right here inside the U.S., TechCrunch’s Manish Singh experiences that India noticed two important raises on this planet of fintech in current weeks:

Indian fintech money View valued at $900 million in new funding

Indian fintech Kreditbee nears $seven-hundred million valuation in new funding

in the meantime, in South Korea, fintech Toss bumped its valuation as a lot as a staggering $7 billion:

South Korean monetary great app Toss closes $405M collection G as valuation rises 7%

completely different funding provides reported on the TC website embody:

Gynger launches out of stealth to mortgage firms money for computer software

Fintech Vint hopes to level out wine and spirits proper into a mainstream asset class

Early-stage Mexico fintech Aviva is making loans as simple as a video name

And elsewhere:

Saudi start-up Manafa raises $28 million to fund enlargement

And, that’s a wrap. I’m not typically one for resolutions however I can say that I am attempting to start this yr off on a extra upbeat observe. final yr was difficult in pretty a little bit of the method, nonetheless it doesn’t assist to be destructive or doom and gloom. there’s nonetheless so a lot good information and issues to be grateful for. So, my want for 2023 is extra resilience and optimism for us all as a outcome of whereas we will’t always administration what occurs, we can administration how we react. Thanks as quickly as extra for studying, and to your assist. I’m always right here to your suggestions! till subsequent week…xoxoxo Mary Ann

0 Comments