Our trendy world has a voracious urge for food for metals, and good buyers can leverage that for income. The guidelines of metals is intensive, and ranges from lesser-acknowledged unusual parts corresponding to scandium, yttrium, and gadolinium to the very important component of every battery in every digital machine, lithium. Lithium has been rising in worth as laptops, ipads, and smartphones, with lithium-ion batteries, have proliferated, however in latest instances the progress of electrical autos – and their far greater battery packs – has pushed the worth of lithium sky-extreme.

From an buyers perspective, this opens up a quantity of avenues for alternative, significantly in lithium mining and lithium processing.

In a report from B. Riley Securities, analyst Matthew Key lays out the current standing and path forward for the lithium commerce: “Lithium has arguably been thought of one of the best-performing commodity for the motive that start of 2021, with current pricing for carbonate and hydroxide at $seventy 4,000/Mt and $eighty,500/Mt, respectively, primarily from battery demand for electrical autos. general, we think about the sturdy outlook for EV gross sales will assist strong pricing over the shut to time period…”

Key’s description displays why now’s the exact time for buyers to ponder lithium, as a portfolio various. So let’s try two lithium shares that the analyst has given buy scores collectively with double-digit upside potential – on the order of forty% or extra. the exact actuality is, Key’s view isn’t any outlier. working the tickers through TipRanks’ database, we obtained here across that every boasts a “sturdy buy” consensus rating from the broader analyst neighborhood.

Lithium Americas (LAC)

First up, Lithium Americas, is creating two fundamental lithium mining and processing initiatives, the Cauchari-Olaroz mine in northern Argentina and the Thacker move mine in Nevada. Thacker move is doubtlessly North America’s best lithium mine, with the most important acknowledged lithium reserves inside the US. Between the two initiatives, Lithium Americas expects to generate roughly one hundred,000 tons of usable lithium yearly.

For now, the agency stays to be in enchancment levels, transferring each initiatives in the direction of completion and the commencement of manufacturing. In its 3Q22 report, launched on October 27, the agency reported continued progress on the Cauchari-Olaroz, with an replace on the manufacturing ramp-up schedule anticipated earlier than the prime of this yr.

Turning to Thacker move, Lithium Americas reported that, by September of this yr, it had despatched one hundred tons of ore from the mine for the manufacturing of product samples that would probably be proven to potential clients and companions. The feasibility research, required earlier than the mine can open, is scheduled for completion in 1Q23.

whereas Lithium Americas stays to be pre-income, it is in a sound monetary place. As of September 30, the agency had readily obtainable $392 million in money and fully different liquid property, collectively with $seventy five million in obtainable credit rating.

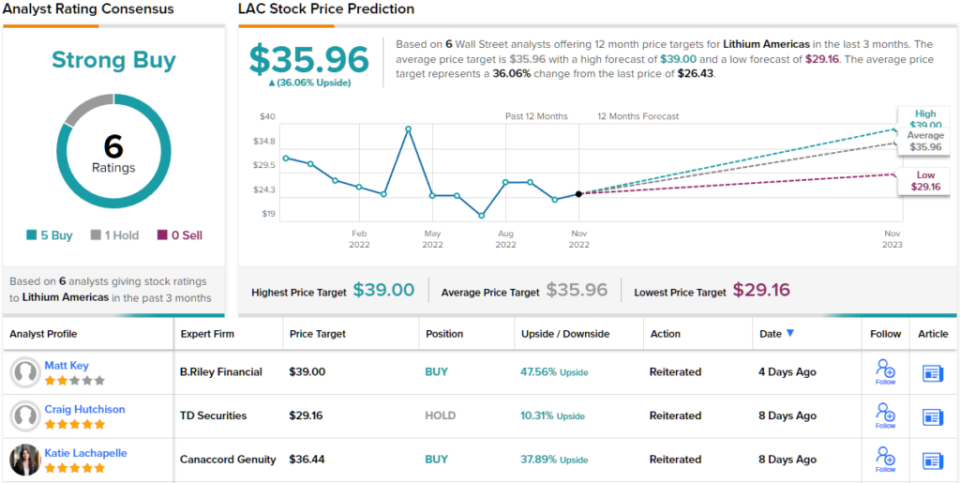

Checking in with B. Riley’s Key, we uncover that he is bullish on Lithium Americas, saying of the inventory: “LAC continues to be thought of one of our favourite names in our safety group, and we think about the completion of Cauchari in early 2023 will function a extreme catalyst for the inventory. Importantly, the rise in shut to-time period carbonate pricing benefited the earnings potential of Cauchari significantly, and we at the second are estimating $332M in EBITDA for 2023E and $385M for 2024E.”

It should be unsurprising, then, that Key expenses LAC a buy. to not level out his $forty one worth goal areas the upside potential at ~forty eight%. (to look at Key’s monitor doc, click on right here)

It’s clear from the consensus rating, a strong buy supported by 5 buy scores out of 6 analyst evaluations, that Wall road is bullish on this lithium agency. As for upside, the shares are buying and promoting at $26.forty three and their $35.ninety six common worth goal suggests a obtain of 36% inside the approaching yr. (See LAC inventory forecast at TipRanks)

Piedmont Lithium (PLL)

the following inventory we’ll have a look at is Piedmont Lithium, a lithium mining and processing agency which, like LAC above, stays to be inside the event course of. the agency’s purpose is to level the US proper into a extreme participant inside the worldwide lithium current chain. It’s a smart purpose; the US has roughly 17% of the world’s confirmed lithium reserves, and with current US manufacturing averaging solely 2% of current current, there’s an excellent deal of room for progress right here.

Piedmont is working to deliver mining property in North Carolina on-line, and its fundamental actions are on the Carolina Tin Spodumene belt, not faraway from Charlotte. the agency holds 1,one hundred acres in that area, and is on monitor to start enchancment actions in 2024. Spodumene focus manufacturing is scheduled to start in 2026, with a purpose of 30,000 tons yearly at full manufacturing performance.

the agency’s fully different fundamental challenge is positioned in Tennessee, the place the agency has chosen a website for a 30,000 ton performance lithium hydroxide plant, with manufacturing focused for 2025. the agency’s Tennessee lithium challenge has just recently been chosen by the US authorities to receive a $141.7 million grant from the US division of vitality, as a component of the Biden Administration’s latest infrastructure regulation.

outdoors of the US, Piedmont has partnerships with lithium mining initiatives in Quebec, on the North American Lithium (NAL) challenge in Val d’Or, and in Ghana, inside the Ewoyaa challenge. Piedmont invested in these initiatives in 2021, and expects to revenue from 168,000 tons annual manufacturing of spodumene focus in Quebec, starting in 2023, and from 30.1 million tons of acknowledged Li2O reserves on the Ewoyaa mine. whereas the Quebec and Ghana initiatives are based mostly on smaller reserves than Piedmont has inside the Carolina, they’re anticipated to log on at an earlier date.

Analyst Matthew Key just recently bumped up his worth goal on Piedmont Lithium’s inventory, and wrote of his dedication: “Our PT for Piedmont elevated for two fundamental causes. First, the rise in prolonged-time period hydroxide prices from $sixteen,000/Mt to $18,000/Mt was extremely accretive to Piedmont’s hydroxide initiatives in Carolina and Tennessee. In complete, the adjustment added roughly $338M in NAV worth for every property. as properly as, the rise in prolonged-time period spodumene prices from $900/Mt to $1,200/Mt additionally benefited the NAV of the agency’s two spodumene property.”

To this finish, Key expenses the shares a buy, and his new worth goal, set at $108, signifies room for ~seventy five% upside potential inside the shares.

general, there are 4 analyst evaluations on this pre-manufacturing lithium agency, and all are constructive, making the sturdy buy consensus rating unanimous. The shares are priced at $sixty one.fifty six and their $108.seventy five common worth goal suggests a obtain of ~seventy seven% inside the following 12 months. (See PLL inventory forecast at TipRanks)

to get hold of good ideas for lithium shares buying and promoting at enticing valuations, go to TipRanks’ best shares to buy, a newly launched machine that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed on this textual content material are solely these of the featured analysts. The content material is meant to be used for informational features solely. it is terribly important to do your particular person evaluation earlier than making any funding.

0 Comments